Author: Emma Lovell, Head of Marketing at Electron

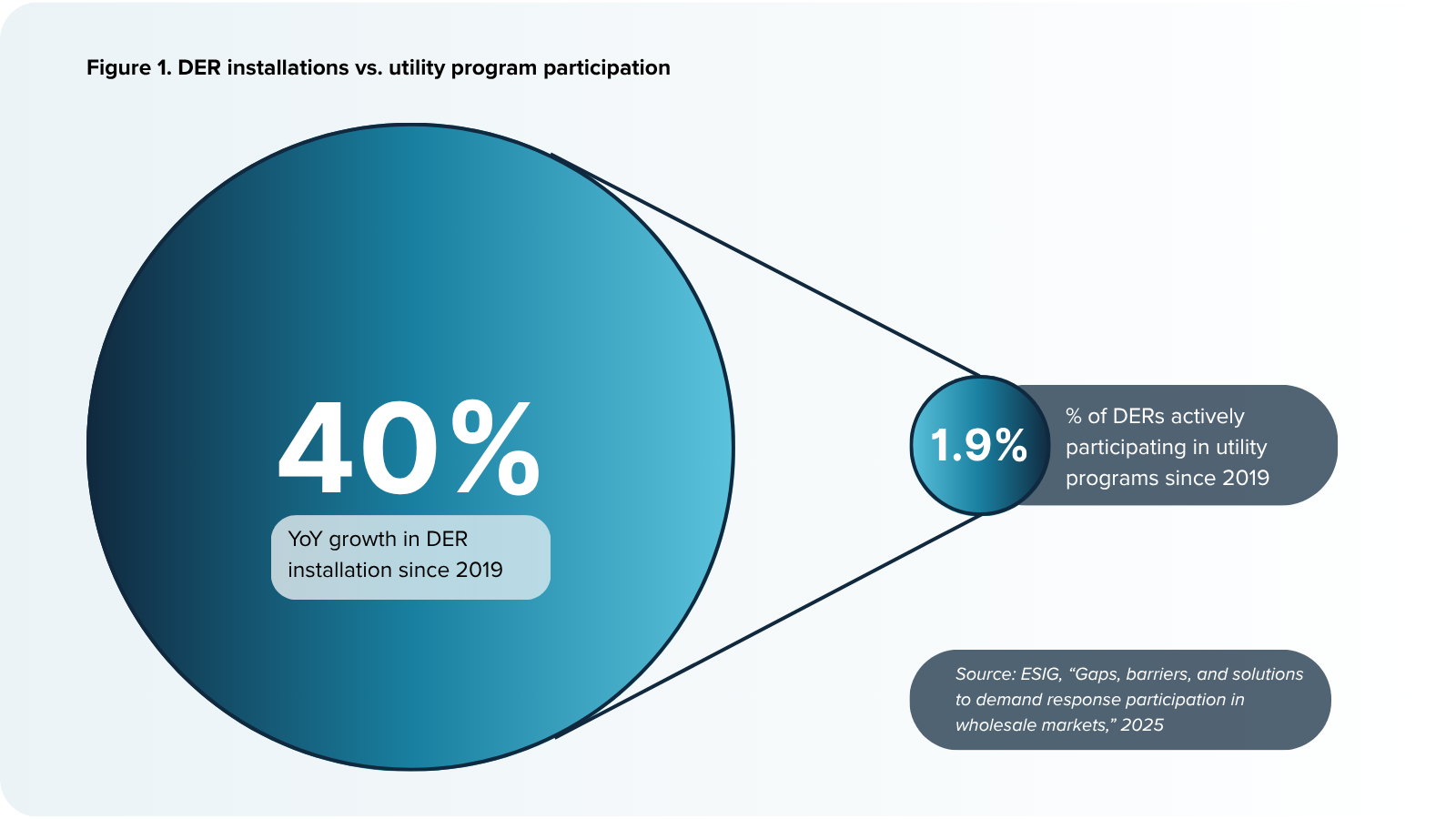

Consumer energy bills are under pressure as distribution-level grid costs grow. CAPEX growth is outpacing inflation whilst regulators increasingly reject rate case applications. Meanwhile, distributed energy resources (DERs) are growing at 40% annually, yet utilities achieve only 2% year-on-year improvements in DER utilisation (see figure 1.).

For utilities caught between rising distribution costs and regulatory pressure to keep consumer bills affordable, traditional grid reinforcement alone cannot solve today’s utility cost management challenges.

The answer lies in strategic DER orchestration that transforms distributed resources from grid challenges into valuable flexibility assets. The question is whether utilities can adapt quickly enough to harness this potential before escalating infrastructure costs become a burden on consumer affordability.

The financial reality

US utilities are facing an unprecedented financial squeeze. Distribution spending is rising faster than inflation, creating a compound effect where each year’s investment requirements exceed the previous year’s by an ever-widening margin.

This trajectory in distribution costs is directly driving up consumer electricity bills at a time when households are already facing broader economic pressures. The numbers paint a picture of the financial transformation underway. Distribution is now the largest capital expenditure category – accounting for 44% of total utility CapEx according to Berkeley Labs, with that growth 2x inflation.

According to analysis from S&P Global, rate case filings have increased over 3x since 2018 as utilities struggle to recover rising costs. Meanwhile, return on equity has declined consistently as regulators prioritise consumer affordability.

The regulatory response

The regulatory landscape has evolved dramatically in response to those consumer affordability concerns. Today’s regulators are – rightly – laser-focused on protecting consumers from excessive rate increases, questioning the sustainability of continued investment while demanding proof of prudent spending. Rate case rejections are becoming more common, encouraging utilities to find more efficient solutions that deliver better value for consumers.

This creates a transformation opportunity. Utilities need to invest more strategically in grid modernisation to manage increasing complexity, while regulators are pushing for innovative approaches that protect consumers from higher bills.

Traditional reinforcement approaches – upgrading transformers, installing new lines, building substations – are reaching their practical limits. These 50-year planning models assume static load growth and predictable consumption patterns, making them incompatible with the dynamic nature that DERs introduce.

Declining returns on traditional infrastructure investments are therefore driving utilities to explore more efficient alternatives that can deliver better service standards while controlling costs.

Technical evolution driving smart solutions

The growth of DERs creates exciting opportunities alongside significant DER integration challenges. Electric vehicles, heat pumps, rooftop solar, and battery storage systems are connecting to the grid at unprecedented rates, each creating potential for innovative grid management approaches rather than traditional reinforcement strategies.

However, a significant participation gap exists that represents massive untapped potential:

- DER installations are growing at 40% annually across residential, commercial, and industrial sectors (see figure 1.)

- Utility program participation is growing at only 1.9% – creating a vast pool of uncoordinated resources (see figure 1.)

- Aggregated DERs can provide resource adequacy at just $5/MW compared to $110/MW for gas peakers and $75/MW for battery storage, according to Brattle Group.

This participation gap represents the difference between DERs being a cost burden and becoming a strategic asset. The challenge is operationalising their flexibility to deliver real grid value. Most DERs today operate independently, creating unpredictable load patterns that force utilities into reactive reinforcement cycles.

But when properly orchestrated, these same resources can provide targeted grid flexibility that defers or eliminates the need for expensive infrastructure upgrades.

The data integration opportunity

The most significant opportunity lies in unifying fragmented utility data systems to enable effective utility operational efficiency to reduce those distribution costs.

DER information is currently scattered across multiple platforms and departments – solar installations tracked in one system, EV charging in another, demand response participants in a third.

Consolidating this information through DER value orchestration creates opportunities for more efficient investment decisions that reduce consumer costs. Consider a neighbourhood with high solar penetration: without coordination, utilities must build expensive infrastructure to handle both peak solar exports during the day and heavy grid draws at sunset.

But with smart DER orchestration, utilities can coordinate battery storage, EV charging, and flexible loads to smooth these patterns.